On 4/2/2026, I watched SBA shares jump $32 in a single day—something rarely seen in cell tower stocks today. These stocks have generally declined over the past five years. Reports suggest SBA is considering selling its tower business. While the industry once delivered consistent high- to low double-digit organic growth, those days are largely gone. Still, the tower business remains highly profitable and continues to attract attention from investors and cell tower consultant professionals evaluating long-term infrastructure value.

Major tower companies lease vertical space, but rising rents on legacy towers have become unsustainable. Carriers are pushing back to control costs, which is compressing revenues for the big three. In many cases, these cost pressures are also influencing negotiations around lease renewal terms and driving discussions about potential lease buyout opportunities to stabilize long-term operating expenses.

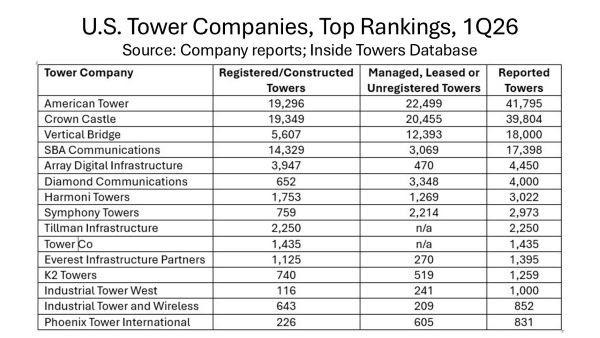

So why suggest Crown Castle or American Tower acquire SBA? The answer is scale. SBA reportedly has 17,464 U.S. sites and adding that portfolio would significantly strengthen either company’s domestic footprint. By comparison, the next largest potential acquisition, Array Digital, has roughly 4,450 sites and that portfolio isn’t as close to SBA.

The case for American Tower to acquire SBA Communications is straightforward. The deal would bring its U.S. footprint to roughly 60,000 towers—less about the number and more about leverage.

With that scale, carriers like Verizon and AT&T can’t avoid American Tower, even amid tense MLA negotiations and high-rent relocations. SBA’s portfolio includes many strategic, hard-to-replace sites, giving added pricing power. It also provides a hedge as T-Mobile is expected to begin evaluating high-rent sites around 2027.

American Tower’s stock has fallen from ~$300 to the $170–$180 range, with growth now resembling the slower, dividend-driven profile of the carriers. While an acquisition would be dilutive, standing still offers limited upside.

Unlike international deals, this is a known asset base—legacy U.S. towers with established rents. SBA has positioned its portfolio well for a sale, and there may not be another opportunity of this scale. The next-largest option, Array Digital Infrastructure, is far smaller and less strategically dense.

This would also be a defining move for new American Tower leadership. Of late, the stock has been relatively flat; this acquisition could establish long-term leadership and widen the gap with Crown Castle. American Tower values being the largest tower owner, and this deal would cement that position. While pushing leverage beyond recent targets would be a hurdle, opportunities like SBA’s portfolio are unlikely to come to market again.

The case for Crown Castle to acquire SBA Communications may be even stronger. Crown recently committed to becoming a pure U.S. tower company, and SBA is the best asset to accelerate that strategy. While SBA has some international exposure, those assets could be sold post-close.

With Crown set to receive $8.5B from its fiber sale in early 2026, the timing aligns well. A deal would also signal that new leadership is fully committed to competing with American Tower. It would narrow the valuation gap and make Crown the largest U.S. tower owner by count at roughly 58,000 sites.

Strategically, SBA’s portfolio offers strong upside. Its sites command high rents, and with carriers targeting relocations away from American Tower, Crown could benefit. Both AT&T and Verizon have MLA agreements with SBA, and while some churn is expected, recent activity suggests American Tower has been the primary target. That dynamic could allow Crown to deepen carrier commitments and drive incremental growth.

More broadly, SBA’s high-quality assets and strong market positioning would enhance Crown’s footprint in key regions. Integration would be complex, but SBA’s performance track record suggests it would become a major long-term cash flow driver.

While a deal involving Crown Castle or American Tower seems unlikely, it would be a major industry moment. After years of layoffs and slower growth, it would inject much-needed momentum. A private equity buyer, by contrast, could bring more cost-cutting and uncertainty.

Who do you think is the most logical buyer—private equity, Crown Castle, American Tower, or someone else?

Need help evaluating your tower agreement, lease renewal, or potential lease buyout? Contact JP Tower Consulting today.